Tags

India: West African demand supports rice bulk freight; container market remains mixed

- West African demand and monsoon disruptions support breakbulk freight

- Container market remains volatile amid frequent GRIs, capacity shifts

India’s rice freight market witnessed mixed trends in the week ended 1 July 2026, as sustained West African demand and monsoon-related operational disruptions underpinned breakbulk freight sentiment. Meanwhile, the container segment stayed volatile, with carrier pricing strategies and frequent General Rate Increases (GRIs) driving divergent trends across East African routes.

West Africa anchors bulk freight

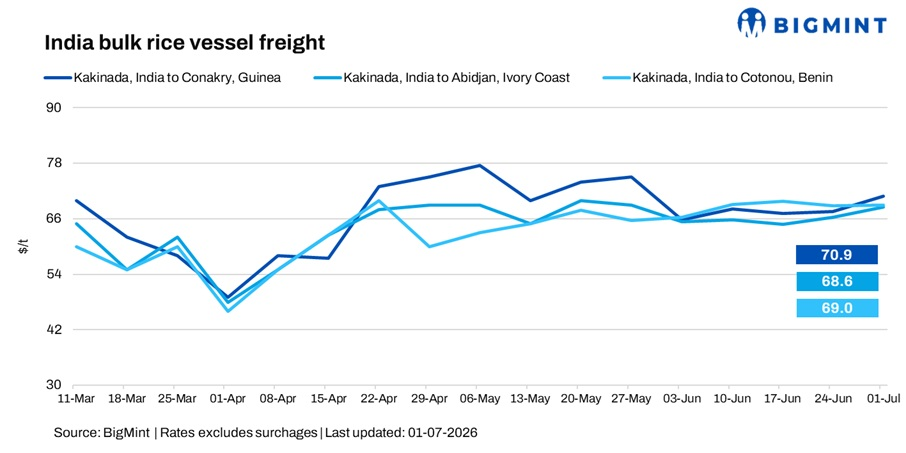

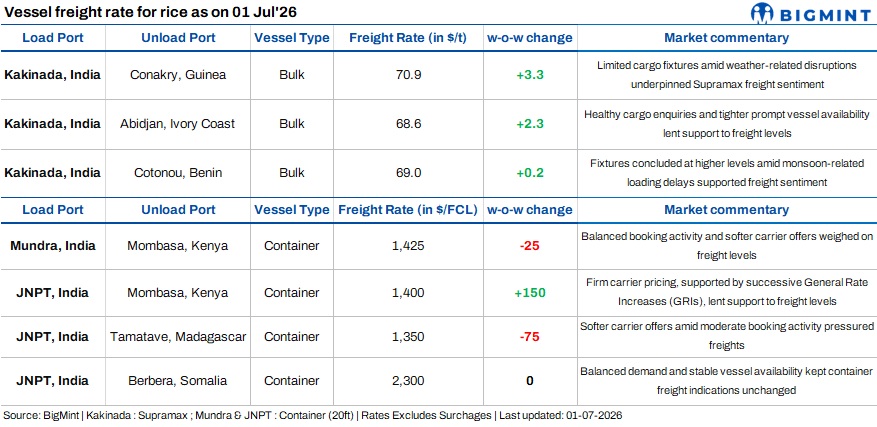

West Africa continued to anchor the bulk freight market, with steady cargo movement towards Benin, Togo, Guinea and Ivory Coast. West Africa continued to anchor the bulk freight market, with steady cargo movement towards Benin, Togo, Guinea and Ivory Coast. Weather-related loading delays and tighter vessel schedules continued to support freight sentiment despite limited fixture activity.

A shipbroker told BigMint, “Some markets tend to slow during the monsoon, while others pick up. At our end, fixture activity has remained relatively slow. We’re hearing freight rates to Cotonou at higher levels at the moment, while the ongoing monsoon is hitting hard, making cargo operations more challenging.”

Another source added, “We’re currently handling smaller shipments, primarily to Benin and Togo. While market activity remains steady, cargo sizes are relatively limited. Operations are currently centred around Kakinada, as securing cargoes from Vizag has become increasingly challenging.”

Route-wise update

Container freight stays mixed

Container freight continued to witness mixed movement during the week. While some East African routes faced competitive carrier pricing, others remained supported by successive GRIs announced by major shipping lines.

A shipbroker said, “The container market is running extremely firm at the moment. Carriers are announcing new General Rate Increases (GRIs) almost every day, keeping freight rates elevated. We expect the market to remain strong through the peak season, with conditions likely to stabilize from October.”

Another market source highlighted the impact of changing vessel deployment patterns, saying, “Freight rates from China and Dubai have risen sharply as most mother vessels are being deployed on China-bound routes, tightening vessel availability and supporting higher freight levels.”

Weather and supply outlook remain in focus

Beyond freight fundamentals, weather developments continue to influence market sentiment. India’s southwest monsoon has advanced across most parts of the country, but rainfall distribution remains uneven, while forecasts of a strengthening El Nino during the critical July-September crop-growing period have kept traders cautious. Weather conditions are being closely monitored, as any prolonged rainfall deficit could affect kharif rice production and export availability later in the season.

India’s comfortable rice inventories continue to cushion immediate supply concerns, limiting any sharp reaction in the physical market.

Non-basmati rice export prices rise 1.5% w-o-w

BigMint’s assessment for Non-Basmati Parboiled Rice FOB Kakinada increased 1.5% w-o-w to $338/t as on 1 July 2026, supported by steady buying interest from African destinations and firmer freight sentiment.

Outlook

Rice freight sentiment is expected to remain firm in the near term, supported by steady West African demand and weather-related operational challenges. Container freight is likely to remain mixed as carriers continue adjusting pricing through GRIs during the peak shipping season. Monsoon progress, El Nino developments, vessel availability and carrier pricing will remain key market drivers in the weeks ahead.

https://www.bigmint.co/insights/detail/india-west-african-demand-supports-rice-bulk-freight-container-market-remains-mixed-765283Published Date: July 2, 2026